Castalia’s blog

The Eastern Africa Power Pool (EAPP) is set to launch a day-ahead market (DAM) in early 2025. This marks a pivotal step toward realizing a functional regional East Africa Power Market. Accordingly, this initiative aims to foster competition, reduce electricity supply costs, and enhance energy security across the region. By enabling day-ahead power trading among its 13 member countries, the DAM will facilitate a more efficient allocation of resources, balancing supply and demand more effectively.

The DAM will serve as a centralized platform where participants can buy and sell electricity at financially binding day-ahead prices. Additionally, this structure is designed to optimize the use of available generation resources, potentially driving down costs and delivering customer savings. Improved price signals can provide clarity on the marginal cost of electricity, encouraging a convergence of regional power prices—although this will depend on mitigating transmission constraints and losses. Without deeper regional integration through significant transmission expansion, the potential benefits of the DAM may remain unrealized.

Work on transmission lines in Nairobi, Kenya

The EAPP must address operational and policy challenges to fully reap the benefits of the DAM

The proposed market holds significant potential for advancing renewable energy integration. However, without changes to entrenched operational and policy challenges, the goals of the DAM may lead to modest gains, mirroring the limited outcomes observed in other power pools, such as the West African Power Pool (WAPP). Furthermore, East Africa’s extensive hydropower and growing investment in renewable projects can be best utilized through a flexible market mechanism. The flexibility allows the management of intermittency and enhances grid stability. With zero marginal cost renewables, the DAM could support a greener, more efficient energy future.

Increased trading volumes within the EAPP could alleviate power deficits in some nations while enabling others to monetize surplus capacity. Can the East Africa Power Market fully realize these benefits without addressing price disparities and making the necessary infrastructure investments?

If you’re working on urban water resilience, you must read Rolfe Eberhard’s new paper on behind-the-scenes conflicts that stoked the Day Zero crisis. Rolfe argues a breakdown of trust and communication failures within the decision-making system exacerbated the crisis. Here are five essential lessons for cities facing water stress:

Start working to build trust and the conditions for sound water management decisions before a crisis happens.

Crises put systems under significant stress, and if trust is already low, rational decisions will be difficult to make. This is especially important for decisions related to water because these decisions often need to be made years in advance.

Establish emotional resonance to build trust.

Technical experts and politicians often speak different languages. Technical experts need to find a way to communicate with political leaders and the public to build trust and understanding and foster evidence-based decision-making.

Be transparent, accessible, and accountable.

Politicians must ensure the public has access to clear and timely information about rainfall, dam levels, water usage, and other relevant data. This helps to build trust and can lead to changes in consumer behavior.

Engage with the public.

The Cape Town crisis showed water management is no longer something that can be handled by a small group of technical experts. Cities need to engage with the public in a meaningful way.

Engage proactively in regional water systems.

Cities are almost always part of a larger regional water system. Cities need to be proactive and collaborative to manage regional water systems with other stakeholders.

Queues form as water rationing begins and Day Zero looms over Cape Town

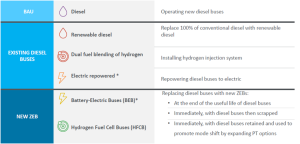

The many options available to New Zealand’s Regional Councils make it difficult to identify the best way to procure new bus service operators. New bus technologies offer substantial opportunities to reduce emissions, but the question is, at what cost? Castalia is very happy to have collaborated with the New Zealand Transport Authority to help guide those councils and bus companies.

Our fully customizable zero-emission bus cost model and accompanying report help Regional Councils weigh the costs and benefits of different bus technologies for bus fleets. Decisionmakers can use the model to easily compare different bus technology options by the total cost of ownership (TCO) per kilometer on a purely financial basis while also considering the impact of greenhouse gas emissions and other harmful emissions from existing diesel buses.

Excitingly, in the process of designing and testing the model, our research revealed that Regional Councils can decrease costs for riders and achieve their climate goals. This is because zero-emissions buses already cost less on a purely financial TCO per kilometer basis than diesel buses. Further, zero-emissions buses have considerable additional health and environmental benefits from the perspective of society as a whole as a result of reduced greenhouse gas emissions and reduced impact of harmful emissions on the health of New Zealanders. Battery electric buses (BEBs) also offer significant financial and emissions savings compared to other bus technologies, including hydrogen fuel cell buses (HFCBs).

Regional Council decision-makers can use the model to easily compare the six most relevant bus technologies for NZ, shown in the diagram below. Crucially, the model also allows regional councils to weigh the costs and benefits of retiring existing diesel buses early, replacing existing diesel buses at the end of their useful lives, or replacing diesel buses on their exiting routes now and repurposing those buses to expand public transport options to induce more Kiwis to use public transport.

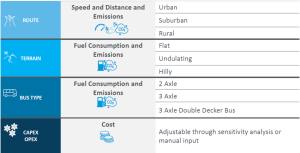

Regional Councils face diverse circumstances from hilly, densely populated Wellington to flatter, more spread-out Christchurch. As a result, the model is designed to be easily customizable to match the characteristics of the routes that the bus must serve.

As shown in the figure below, the model evaluates three types of routes with three terrain options for three different bus sizes. It also allows for conducting sensitivity analysis on key inputs such as fuel cost and bus capital cost.

Regional Councils face diverse circumstances from hilly, densely populated Wellington to flatter, more spread-out Christchurch. As a result, the model is designed to be easily customizable to match the characteristics of the routes that the bus must serve.

As shown in the figure below, the model evaluates three types of routes with three terrain options for three different bus sizes. It also allows for conducting sensitivity analysis on key inputs such as fuel cost and bus capital cost.

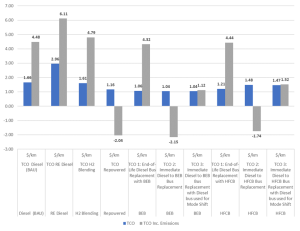

The figure below shows an actual dashboard output for a sample scenario for two-axle buses on an urban, high-density, short-distance bus route over flat terrain. The figure shows the TCO per km of different bus technologies with and without considering the cost of emissions.

The light blue bars, which show the TCO per km without considering the cost of emissions, show that BEB is the least expensive technology at $1.04 per km. Further, the figure shows that it is least expensive to either retire diesel buses immediately and scrap them or use them to induce “mode shift” rather than replacing them at the end of their useful life.

When the model does consider the cost of emissions—represented by the grey bars in the figure below—replacing diesel buses with BEB immediately and scrapping the existing diesel buses is the least cost option on a TCO per km basis. In fact, the TCO per km is negative when considering the cost of emissions because the model accounts for the value of the avoided emissions that come from scrapping the diesel bus early. Hence, the social value of health and environmental costs avoided by taking a diesel bus off the road early completely outweigh the cost of buying and operating the new BEB.

*The negative number for TCOs where existing diesel buses are replaced early reflects the finding that the health and environmental benefits of replacing diesel buses early are so great that they outweigh the costs of operating the bus compared to the BAU.

We look forward to working with interested parties to apply this exciting new model and share the results of our work!

The Study Report and the model are both available in New Zealand Transport Agency’s website.

The Study Report is available here: Zero Emissions Bus Economic Study

The model is available here: Zero Emissions Bus Model

Read more about our transportation work:

Hydrogen Modelling Study in New Zealand

Feasibility and Structuring of Ninh Binh—Bai Vot Expressway, Vietnam

Read our other posts: